Should you refinance your home? Strategic reasons and lesser known truths of refinancing that everyone needs to know.

People have been talking about refinancing these days. Some have taken action - just ask any lender, they’ll tell you that they’ve been doing more refinancing than purchases this winter.

It makes sense. There was a period of time where interest rates hit 8% (October 2023, I believe), as compared to today’s low 6%. There is now enough of a spread to ask, “Is now a good time to refinance?”.

Ask Google that and you’ll get a generic answer like being able to reduce monthly payments, change a loan type from an adjustable-rate mortgage (ARM) to a fixed-rate loan, remove a co-borrower after a life change etc.

Yes, all valid, but I’m not here to talk about necessary moves.

Let’s talk strategy, and let me share some truths about refinancing that isn’t widely discussed.

Strategic moves to refinancing

People generally make strategic refinancing moves within the first 5 years of the loan, because those initial 5 years are when one has hardly made a dent in equity.

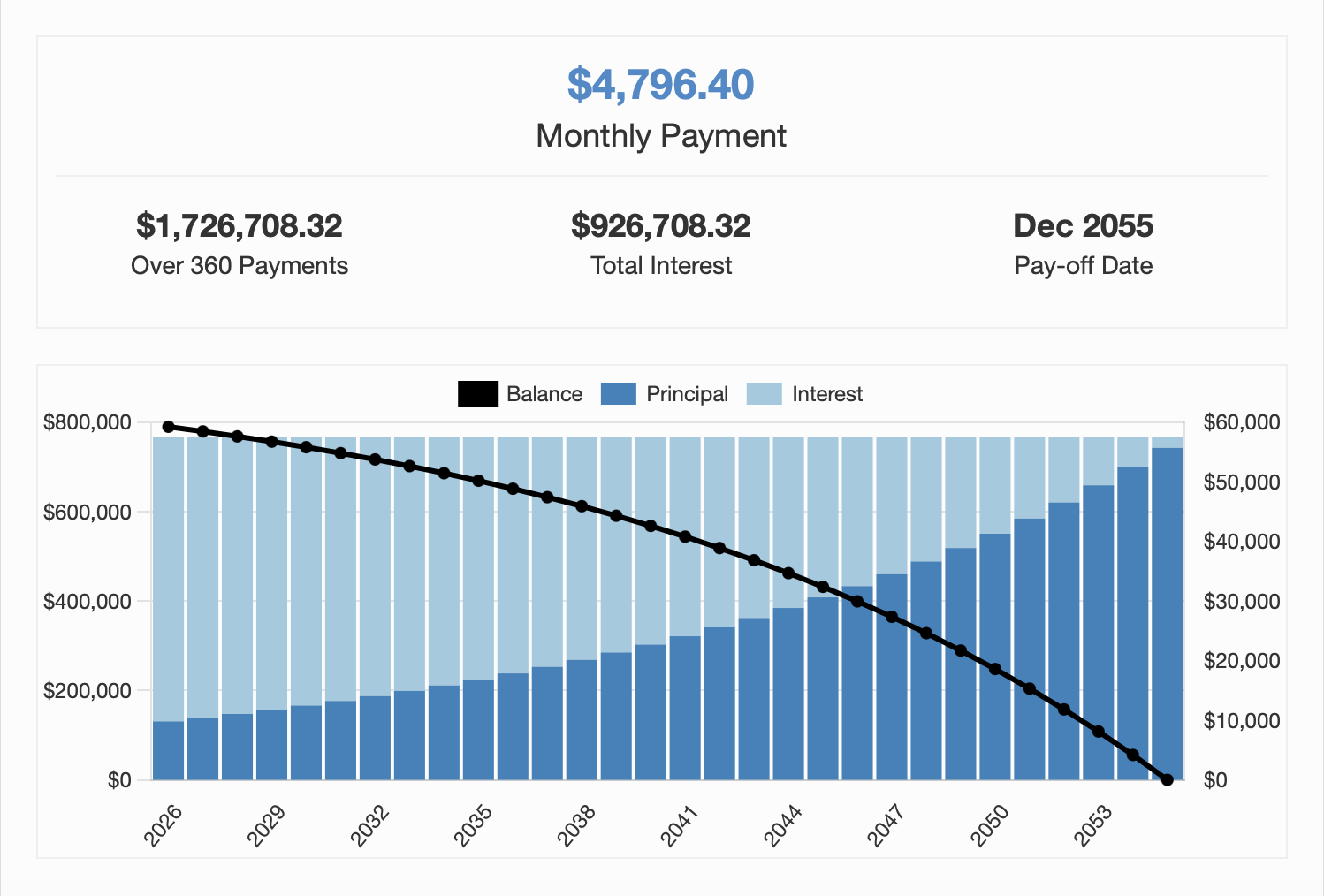

Here’s what an amortization graph and schedule looks like for an $800,000 loan at 6% over 30 years:

Year 1: Principle is 17% of total payment. Year 4: Principle is 20% of total payment. Perhaps that “20” makes people think that they’ve finally got real skin in the game.

2 strategic reasons to refinance:

1. Monthly savings and ability to recover closing costs in less than 3 years.

Don’t just focus on the monthly savings and forget that there are costs to closing: attorney fees, recording fees, lender’s title insurance etc. Closing costs typically start at $2,500.

As a general rule of thumb, multiply your monthly savings by 12, then by 3. Is this sum less than your closing costs? Saving $100 a month while spending $2,500 in closing costs means that you’d have only recouped your closing costs after 2 years of payments.

2. Cash out on equity; leverage equity to grow.

Draw on your home’s equity, because it’s quicker to access that amount than it is to save. Of course, the assumption is that whatever interests you’re making on that cash-out refinance is less than your gain from say, investing in the S&P 500.

A cash-out refinance allows one to draw up to 80% (sometimes 85%) of a property’s value.

Here’s a case example on how to calculate:

5 years ago, you bought your home for $1,000,000. You made a 20% downpayment and took an $800,000 loan

Today, the balance on your loan is $750,000

The value of your house is now $1,100,000

80% of $1,100,000 = $880,000

Amount that you can draw: $880,000 - $750,000 = $130,000

refinancing truths that you should consider

1. The amortization schedule resets when you refinance.

That means going back to that initial mix where only 17% of your payment goes towards your principal.

2. There is no such thing as a free refinance.

There is no free lunch in this world; especially not in America. Believe me, there is an asterisk attached to “free”. For one, there is an attorney involved who needs to get paid and registry fees for the recording. Two, “free” could mean no lending costs, but are you certain that the interest rate offered will be as competitive as the average of 3 other lending quotes?

A free refinance is a red flag. 🚩

3. There is a no-cost refinance.

Yes, there’s a difference between “free” vs “no-cost”, and it’s called “disclosure”. A “no-cost refinance” is an industry term, and it means that the borrower can pay nothing out of pocket upfront. It’s an option to wrap costs into your loan, reflected in a higher interest rate.

4. A new lender’s title insurance is required at each refinance.

If you’d bought your home with a loan, you may recall paying for two title insurances: owner’s title insurance, and lender’s title insurance. When you refinance, you need not purchase the owner’s title insurance again, but you’d be made to purchase the lender’s title insurance.

Tip: Attorneys are the ones who issue title insurances. Check with the attorney who did your closing at purchase- you might be offered a discount on the new lender’s title insurance if you choose to work them on your refinance.

5. Refinancing is not the only way to remove private mortgage insurance (PMI). A reappraisal works too!

If you’ve bought in a town that has strongly appreciated, you need not go for a refinance in order to remove your PMI. Ask for a reappraisal instead- it’s a ~$600 appraisal fee as compared to $2,500+ in closing costs. With luck, you could even be granted an appraisal waiver through the lender’s automatic underwriting system and pay nothing for the reappraisal.

6. The economy is cyclical. Is now the best time?

Do you know where we are in the current economic cycle? Does research point to a recession within the next 3 years where interest rates will fall? If so, would it make sense to delay the refinance?

This article is written with help and input from Katherine Castro-Eardley from Radius Financial, of whom I’ve known for years and worked with on the purchase of my personal home. Please feel free to reach out to her if you’d like an honest assessment of your financials.

Cheers to your financial future.

Acknowledgements

Katherine Castro Eardley

Branch Manager, radius financial group

Email: kcastro@radiusgrp.com

Mobile: 978-973-7115

Reviews